1031 Police Code Unveiled: How It Defines Property Reuse and Guides Urban Transformation

1031 Police Code Unveiled: How It Defines Property Reuse and Guides Urban Transformation

When city planners, developers, and law enforcement intersect, one term often stands out: 1031 Police Code. Though its origins lie not in streetology but in real estate policy, this code has quietly emerged as a critical reference in the language of urban development and legal property transitions. Officially documented under Law Enforcement Code 1031, it captures a specific legal mechanism allowing property owners to exchange one taxable real estate asset for another “like kind,” deferring capital gains taxes in the process.

Used with precision, it bridges financial strategy and enforcement practice, offering a clear framework amid complex real estate maneuvers.

At its core, 1031 Police Code defines a legally grounded process where property transactions comply with specific tax deferral rules. While originally rooted in IRS guidance on like-kind exchanges, police code references reflect its application in urban contexts—particularly where city authorities monitor development, zoning compliance, and tax liability linked to property reuse.

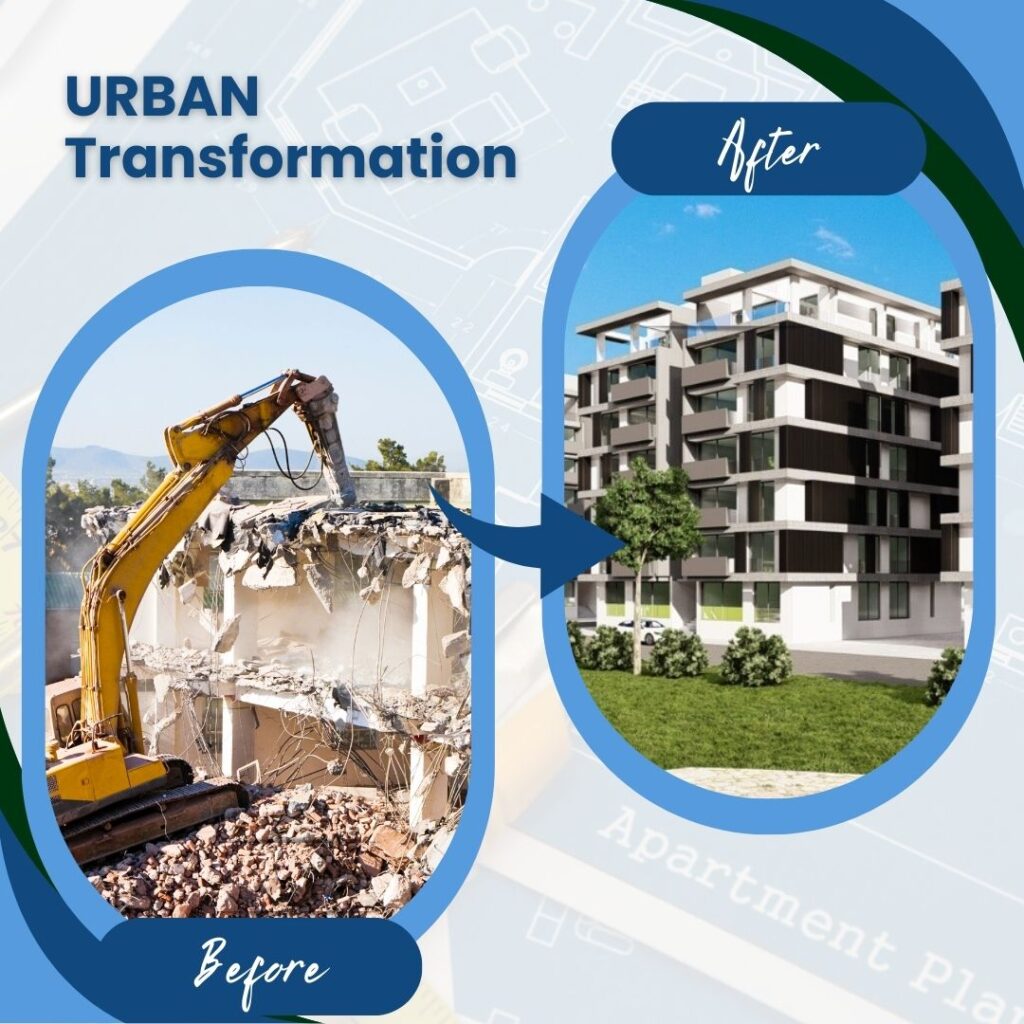

The code ensures that when a building is sold and replaced with another of similar use—say, an industrial warehouse replaced by a mixed-use development—taxpayer gains are deferred rather than immediately realized. This makes 1031 Police Code not just a financial tool, but a regulatory checkpoint embedded in municipal oversight.

Breaking Down 1031: What It Actually Means for Property Owners

The code derives its name from IRS Section 1031, which permits tax deferral when real estate is exchanged “like-kind.” But in a police code context, this aligns with statutory provisions enabling tax-free conversions under strict conditions. Typically, the exchanged properties must share the same primary use—residential for residential, commercial for commercial—ensuring no speculative arbitrage under the guise of reuse.For example, a construction firm selling a warehousing facility for a retail space may invoke this provision, provided the new property qualifies as “like kind” under tax law.

Key components of 1031 Police Code use include:

- Like-Kind Requirement: Properties must functionally serve the same purpose—residential, commercial, agricultural, or industrial. Land for apartment buildings can swap with commercial shopping centers, but trees on land cannot exchange hands under this rule.

- Exchange Process: Both properties must be identified and agreed upon within a strict timeframe—typically 45 days for listing and 180 days for closing—ensuring procedural rigor.

- Tax Deferral Not Exemption: While gains aren’t paid immediately, future sales of the new asset trigger taxation without the deferral.

This maintains the policy’s intent of encouraging long-term reuse, not speculative holding.

- Authority Oversight: Real estate transactions governed by 1031 Police Code often require municipal or regulatory validation, especially when linked to zoning changes, urban renewal, or public infrastructure projects.

In practice, this means a developer purchasing a vacant lot for a new supermarket may sell an older storage unit, and if both are deemed “retail-type lucanokeiten,” the tax burden is shelved—not eliminated. The deferred revenue later becomes part of the city’s tax base when the new asset is sold, aligning private investment with public fiscal planning.

The Role of 1031 Police Code in Urban Development and Compliance

Beyond individual transactions, 1031 Police Code functions as a regulatory anchor in urban renewal and enforcement. Municipal governments leverage it to guide redevelopment in blighted areas, where tax-deferred exchanges incentivize the revitalization of industrial zones into residential hubs.By clearly defining what qualifies as “like-kind,” the code reduces ambiguity in permitting, ensuring only legitimate reuse qualifies

Related Post

Discovering Telegram Viral Videos Free: Your Ultimate Guide to Sharing the Unseen

How Many Days Are Left in 2025? Exact Count Revealed Before Year Closes

Exploring Janelle James' Husband: A Deep Dive Into Their Relationship

Unraveling the Cosmos: The Real Identity Behind Beri Galaxy